")

Upside Investing represents a revolution in investment/spending strategy. It lets you set a living standard floor that only rises as a result of investing in stocks and other risky assets. The higher your floor, the lower your upside and vice versa.

The stock market is, once again, going nuts — dropping relentlessly, then bouncing back, only to plunge again, but then recovering, well, kind of, and …

This is, in short, excruciating times for those counting on the market to see them through retirement. Stocks have always been a high-reward, high-risk ride. But since the Great Recession, the market seemed reliable. No longer. Today’s economic and geopolitical world is crazzzy and the stock market doesn’t like crazzzy.

We now face raging inflation, round three of COVID, lingering supply-chain disruptions, on-again-off-again Chinese production, global energy and food shortages (curtesy of Vladimir the Excrement), an increasing probability of war with Russia, an ongoing trade war with China, a decent short-term chance that Chinese will invade Taiwan, Iran’s closing in on a nuclear weapon, the potential for economic boycotts of red states thanks to Roe’s repeal, an economic hurricane (Jaime Diamond’s stupid word) supposedly heading straight at us, and the Fed threatening to shoot the economy in the head.

Wall Street’s Con Job

Most of us know enough not to invest our life’s savings playing craps at Caesars Palace. The stock market’s also a casino. So, why are most of us who can playing it? Because it’s the best casino ever — one with a terrific average return. Yet it comes with huge risk. (I reference here investing just in the stock market. But they are largely a stand-in for the entire array of risky investments, such as long-term nominal bonds, foreign stocks, commodities, land, crypto currencies, foreign currencies, etc. But to keep things simple, let’s just think about two assets — stocks and inflation-indexed Treasuries.)

The really big question: How can we play the market, especially these days, without potentially getting badly burned?

Wall Street claims to have found this Holy Grail. It’s called the bucketing strategy. It relies on stocks being safe in the long run. The idea is to buy stocks and put them in a bucket that you keep for retirement. Since “stocks are safe in the long run,” when you retire, you’ll find your bucket is worth multiples of your initial investment, ensuring a lucrative retirement.

There’s just one problem with this strategy. Stocks aren’t safe in the long run. On the contrary, the longer you hold your bucket, the more time it has to lose value. Zvi Bodie, Boston University’s distinguished emeritus finance professor, whose undergraduate finance text (co-authored with Nobel Laureate Robert Merton), entitled Finance, is used in most business programs across the country, has spent years debunking Wall Street’s dangerous fantasy. Yes, the more you invest in stock, the greater the chance of ending up with a very high cumulative long-term return. But your chance of losing your shirt and doing so early on, at that, also rises.

Stocks Aren’t Safe in the Long Run

Consider spending $100,000 today on a zero-coupon, inflation-indexed Treasury bond that pays nothing for 30 years and $132,797 in today’s dollars in year 30. (Note, such zero-coupon bonds are available only on the secondary market.) This is a perfectly safe 30-year investment.

Next consider investing the $100,000 in the S&P, instead, and cashing out in 30 years. On average, your investment will grow in real terms by 9.5 percent. But every year, the typical spread on that 9 percent will leave you earning negative 11 percent or positive 29 percent. And that’s just the standard 20 percent deviation. Annual losses (gains) can be far larger. No surprise. The stock market is a random walk with a drift — the 9 percent average annual increase. (Yes, there is some reversion to the mean, but it’s small and, arguably, temporary.) And random walks can head off in all kinds of directions, including downward directions.

But, you say,

Over 30 years, that drift makes it highly likely that I’ll end up with far more than $132,797 in 2052.

My answer:

Stuff happens. And nothing guarantees your thirty-year nominal stock return won’t equal the negative 39 percent nominal return the Japanese stock market generated between 1990 and 2020. That would leave you with just $61,000 in 2052. And if the next thirty years see the same cumulative inflation as the last thirty, your $100,000 will be worth $26,872 in today’s dollars — miles below the $132,797 had you played it safe.

But, you respond:

The U.S. is not Japan. Over all 30-year periods from 1926 to the present, the U.S. stock market has yielded an annual return of at least 8 percent.

My response:

First, you need to adjust for inflation. Once you do so, the 8 percent minimum 30-year annual stock return is only 0.5 percent. Second, the U.S. data provide only three independent, 30-year cumulative-return data points. Studies that reference “all” 30-year periods are using the same annual return data over and over again. That’s not statistically kosher. Third, the U.S. stock data suffer from survivor bias. We don’t have data on stock returns from countries that didn’t survive the test of time or whose stock markets were closed during periods of occupation or regime change.

The Deeper Problems With the Bucketing Strategy

In persuading the public that stocks are safe long-term, Wall Street is giving people license to spend more and save less as they head to retirement. If their bucket of stocks turns out to be full of holes, they’ll reach retirement not only with an empty or half-empty bucket, but with less in the way of other assets. Moreover, in saving less, bucketers will likely end up putting less in the market than would otherwise be the case. Not adding to your bucket of stocks is akin to withdrawing from your bucket. It generates what’s known as sequence of return risk. This is the problem of taking money out of (not adding money to) the market and, consequently, having fewer assets invested when returns are positive.

Last point. Suppose you just retired with a bucket of stocks you’ve been accumulating for the last thirty years. So far this year, the market has dropped 20 percent. That’s evidence, as plain as day, that there is nothing safe about bucketing. If all your resources were invested in stock, you just suffered what, on average, is a 20 percent drop in your living standard for the rest of your days. This hurts far more than a 20 percent gain helps. I.e., people are what we economists call risk averse, meaning they care far more about the downside than the upside. But The Bucketing Strategy is all about the average cumulative return, not the dispersion in the cumulative return, let alone the far greater dispersion in personal well-being associated with the dispersion in cumulative return.

Upside Investing — The Real Way To Invest Safely In the Stock Market

My company just launched Upside Investing as part of its economics-based, lifetime, financial planning software tool — MaxiFi Planner. Upside Investing lets you set a base living standard floor and experience only upside risk from investing in the stock market. Upside risk means being able to permanently afford and enjoy a higher living standard. (Living standard references your discretionary spending per adult with adjustments for economies in shared living and the relative cost of children.)

This sounds impossible. How can you floor your future living standard — make sure it doesn’t fall below a base level — while investing in the stock market, which, I’ve just argued, is unsafe over any duration?

The answer is found in a 2500 year-old saying attributed to Aesop — Don’t Count Your Chickens Before They Hatch. In this context, it means don’t spend out of your stocks until you have converted them to safe assets. This is how most of us go to the casino. We leave our wallets in our hotel rooms (that secures our living standard) and only spend our winnings, if there are any, after we’ve left the casino.

Upside Investing— a Joint Spending-Investing Strategy

As I’ve indicated, the Bucketing Strategy encourages spending out of risky assets. Upside Investing does the exact opposite. The joint spending-investing strategy could not be simpler. Let me describe it in four steps.

- You tell MaxiFi how much you have in stocks, how much and when you will add to your stocks, and the ages (e.g., 60 to 75) during which you will gradually convert your stocks to safe assets (e.g., Treasury Inflation Protected Bonds).

- MaxiFi builds a Base Plan assuming all money invested in stocks is lost but that your other investments are safe. This establishes your base discretionary living-standard floor and the associated total annual discretionary spending — all predicated on your losing every penny you have in the market.

- Next MaxiFi simulates 500 paths of stock returns. Along each path, you spend at your base floor level until you start converting your stocks (if they still have value) to safe assets. With each conversion of stocks to safe assets, MaxiFi permanently raises your discretionary living standard floor.

- MaxiFi shows your base living standard floor and the range of living standard increases you may experience.

To summarize, you set your stock investments by simply determining how much to put in the market. What’s left of your resources is used to build your base living-standard floor. You raise your floor, and thus your annual discretionary spending, as you convert your stocks to safe assets. Before then, you spend assuming your bucket of stocks is or will become worthless. This is what I mean by saying Upside Investing is a combined investing-spending strategy.

Illustrating Upside Investing

Consider 40-year old Jane. She’s single, lives in Oregon, earns $200K a year, pays $24K in annual rent, has $250K in regular assets, and $1million in her IRA to which she contributes $20K annually. (Earnings and rent keep pace with inflation.)

Jane can invest safely at 1 percent real in 30-year TIPTIP -0.2%S. If she invests nothing in stocks, her real annual discretionary spending is $72,621.

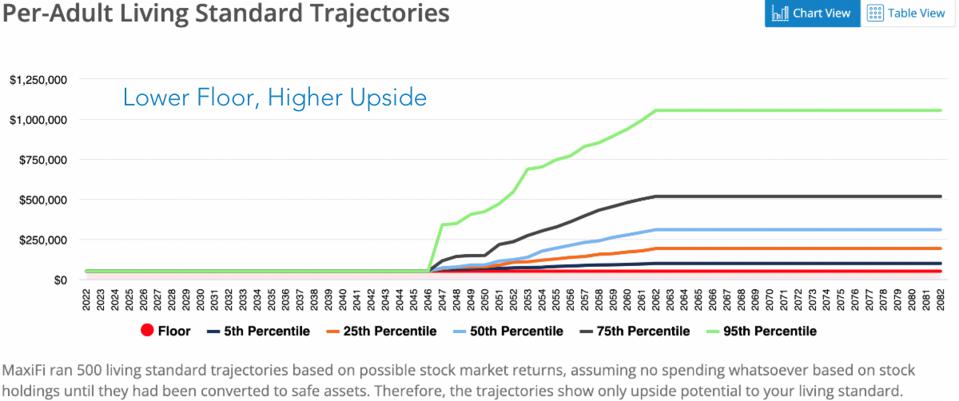

If, instead, Jane invests 80 percent of her regular and IRA assets and as well as 80 percent of her future IRA contributions in stock, her base discretionary living standard floor falls to $49,880. But as the figure below shows, Jane can experience a considerable living standard upside as she converts whatever her stocks generate to safe assets between 65 and 80. (At 65 she converts 1/15th of her stocks, at 66 she converts 1/14th, etc.)

Jane Invests 80 Percent in Stocks, But Spends Only Out of Safe Assets

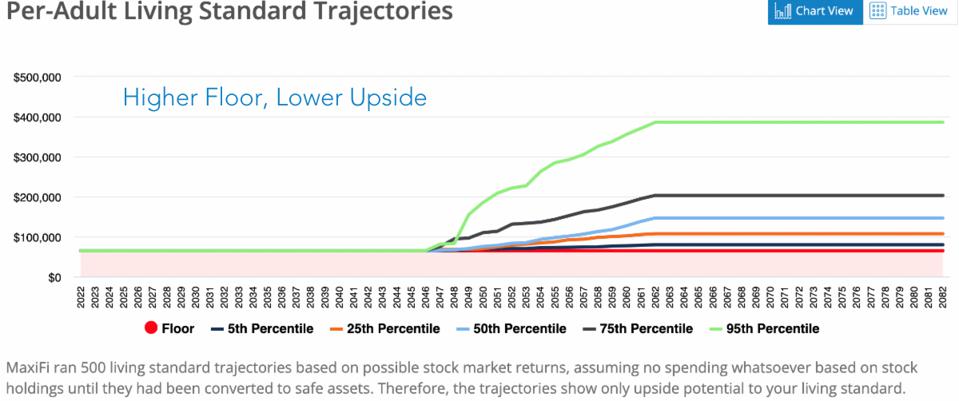

Next, suppose Jane invests 20 percent of her assets and future IRA contributions in stock. As the next figure shows, Jane’s base living standard floor is now higher––$64,922. But her upside is considerably lower. For example, Jane’s 75th-percentile trajectory (the trajectory producing the 75th highest level of lifetime spending) ends up at just $203,168 rather than $516,485 when she invests 80 percent in the market.

Jane Invests 20 Percent in Stocks, But Spends Only Out of Safe Assets

Upside Investing — The Real Holy Grail, a Recap

- Invest in stocks, but don’t spend from them until they have been converted to safe assets.

- The more you invest in stocks, the lower your living standard floor, but the higher your upside.

- The less you invest in stocks, the higher your floor, but the lower your upside.

- Investing even a relatively small share of assets in stocks may deliver substantial upside.

- Controlling living standard risk depends not just on how aggressively you invest, but on how aggressively you spend.

- Prior to converting your stocks to safe assets, you avoid sequence of return risk (ending up with less money in stocks due to mis-timing withdrawals prior to converting to safe assets). This explains why Upside Investing provides significant upside potential.

Can You Do Upside Investing On Your Own?

If you’re Jane, why do you need MaxiFi Planner to do Upside Investing? Can’t you just put some money in the market, let it ride, and start taking it out at, say, 65, continuing through, say, 80?

Not really. You need to compute your baseline living standard floor in order to know how much to spend and save (in a safe manner) this year and through time. You also need to see the range of living-standard upsides you’ll potentially experience based on different choices of your base floor (choices of how much to put in the market). Otherwise, you won’t be able to make a reasoned decision on how much to put in the market.

This is not something anyone can do with Excel or some other spreadsheet program in an afternoon. The amount of technology underlying the figures presented above is simply enormous. MaxiFi’s computation engine received a patent for its method of iterative dynamic programming. The tool was developed over 29 years by a team of expert software engineers and economists. It incorporates incredible detail concerning federal and state taxes, Social Security benefits, and Medicare Part B premiums. Just the efficiently-crafted code for Social Security comprises a ream of paper were it to be printed out.

Finally, if you are using TIPS (Treasury Inflation Protected Securities) as your safe asset in effecting Upside Investing, you’ll need to ladder your purchases. This FAQ at maxifi.com lays out how this can be done in practice. As you’ll read, MaxiFi computes the annual net withdrawals of safe assets needed to be indemnified (covered) by TIPS of different maturities. These annual net withdrawals are calculated precisely by the program.

0 Comments