")

Tax reform championed by Donald Trump and passed by a Republican Congress was a boon for middle-income families. According to a study by the Atlanta Federal Reserve Bank, the average household in America can expect a lifetime gain of about $25,000.

And despite persistent claims that the measure was a giveaway to the rich, the percentage gain was roughly the same for every income class. If anything, the current tax code is more progressive than the one it replaced.

Yet more needs to be done. We need to remove the most unfair, most anti-work, most anti-saving provisions of the tax code – ones that burden the middle class. What follows are some examples.

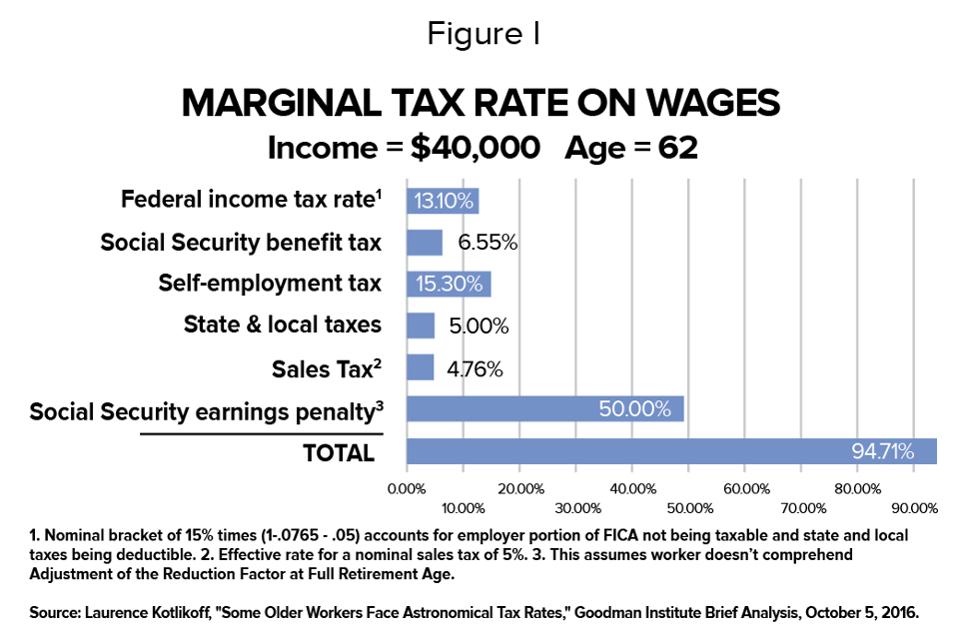

Liberate older workers. Roughly 90 percent of seniors begin collecting Social Security benefits before they reach the full retirement age. Yet if these folks get a new job or a part-time job and earn one dollar more than $17,640, they will lose 50 cents of Social Security benefits because of the earnings penalty – a draconian tax enforced by the IRS. For a $20-an-hour employee, the tax kicks in if you work Monday, Tuesday and half of Wednesday.

When Social Security’s earnings penalty is combined with the Social Security benefits tax and other taxes, middle-income, senior workers can lose as much as 95 cents of every dollar of wages – the highest tax rate in the nation. [See Figure I.]

Credit: Goodman Institute HTTP://WWW.GOODMANINSTITUTE.ORG/WP-CONTENT/UPLOADS/2016/10/BA-115.PDF

Widows with children trying to get by on Social Security survivors’ benefits also face a 50-percent earnings penalty. Negotiating the tough tradeoff between the demands of parenthood and the demands of work is hard enough in its own right. Let’s get government out of the way.

These taxes are unfair. They also make no sense. A study produced by the Goodman Institute for Public Policy Research estimates we could abolish the earnings penalty tomorrow without any net loss of revenue for the government.

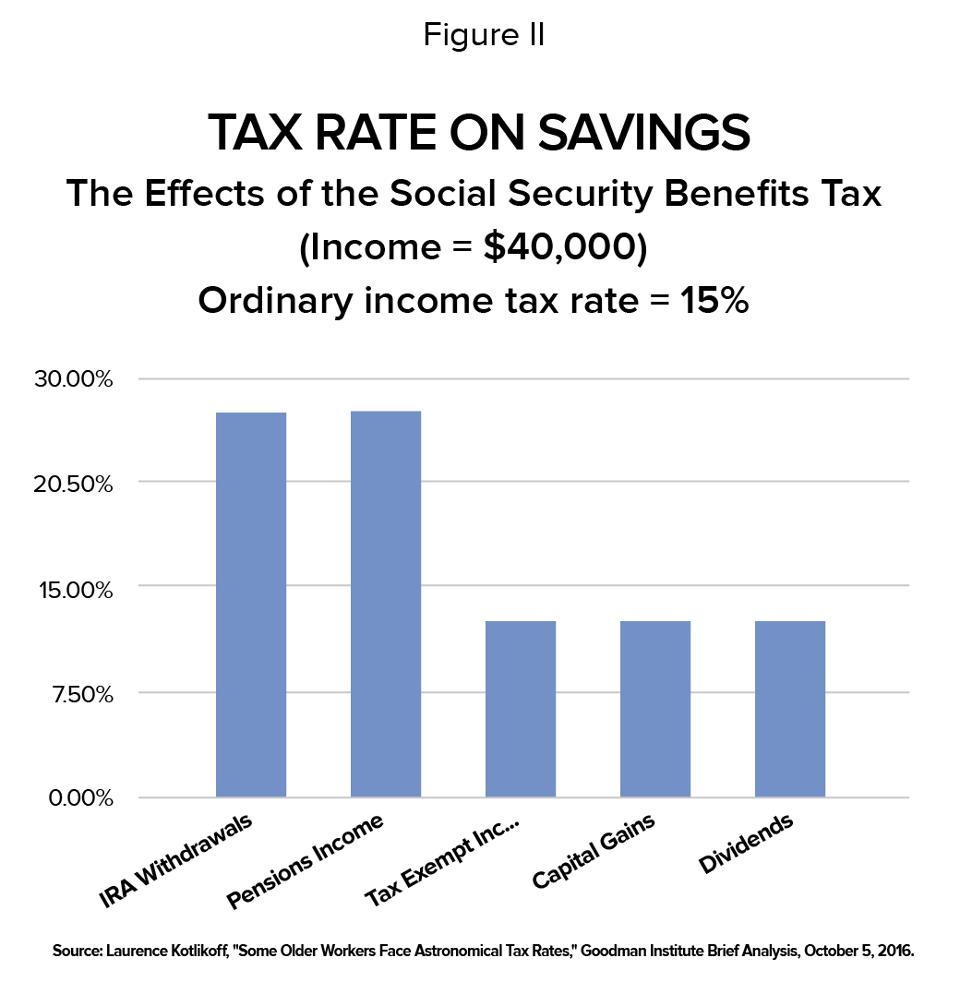

Liberate older savers. The Social Security benefits tax is a misnomer. If a senior has only Social Security income, no tax is owed. The tax kicks in only when there is other income. Because of this tax, seniors can pay almost double the tax everyone else pays on pension income and IRA withdrawals and significantly higher taxes on capital gains and dividend income. They also pay taxes on “tax exempt” securities – taxes that no one else has to pay. [See Figure II.]

Credit: Goodman Institute HTTP://WWW.GOODMANINSTITUTE.ORG/WP-CONTENT/UPLOADS/2016/10/BA-115.PDF

Like the earnings penalty, a tax on non-Social Security income is not paid by the rich or the poor. It is a middle-income-earner tax.

Another provision that needs to go is the practice of forcing seniors to withdraw funds from their savings accounts at age 70½. Funds in IRAs, 401(k)s and other tax-sheltered accounts are a source of capital that funds investment, creates jobs and produces higher wages for workers. Why are we forcing seniors to take this money out of the capital market, give part of it to the federal government, and probably consume whatever is left?

Liberate the self-employed. Independent contractors (e.g., Uber drivers) and owners of home-based businesses (most of whom are women) are discriminated against under current tax law. They do not get the same tax relief when they purchase health insurance, save for retirement, pay for day care or pursue other “employee benefits.” The goal should be labor market neutrality. People should be treated the same under the tax law – whether they work for themselves or work for someone else.

Bring Medicare into the 21st century. Instead of trips to the doctor’s office, why can’t seniors talk to doctors by phone or email – the way many non-seniors do? Instead of trips to the emergency room at nights and on weekends, why can’t they have access to Uber-type house calls? Why can’t they have a concierge doctor (which in some places costs only $100 a month) instead of trying to decipher the complexities of Medicare’s complicated fee-for-service system?

One solution is to let Medicare make a deposit to a tax-free Health Savings Account (HSA), provided the senior is willing to take responsibility, say, for all primary care. Beneficiaries could then take advantage of the best services the market has to offer. Right now, seniors are the only citizens who are not allowed to have an HSA.

Bring laws affecting working families into the 21st century. If employees already have health insurance through a spouse’s employer, why can’t they trade health insurance for higher pay? Believe it or not, this is another income tax problem. An employer who lets even one employee choose between taxable wages and a nontaxed benefit risks having the IRS declare all the employer’s benefits taxable to all the employees. Does anyone think that makes sense?

Why does a housewife who takes a minimum wage job get immediately put into her husband’s much higher tax bracket? Why can’t husbands and wives get equal credit for their Social Security payroll taxes, the same way they share contributions to other savings plans?

These provisions of our tax system were created years ago when Congress thought husbands would go to work, wives would stay home, and they would never get divorced. It’s time to bring the tax law into the modern age.

Another opportunity is to double the child care tax credit. Economist David Henderson has shown that this is a tax relief measure that pays for itself. If working mothers can afford more child care, they will work more hours, earn more money and pay more in taxes to the federal government.

These are just a few of the changes we need to make our tax system work better for seniors, for women and for working families.

0 Comments