")

By John C. Goodman

Originally posted on Forbes, October 2015

Here is the good news. Responsibility for managing health care spending is being increasingly shifted away from third-party payer bureaucracies to individual patients, who often are much better at evaluating the costs and benefits of their own care.

Here is the not-so-good news. Although the responsibility is being shifted, much of the time insurance dollars are not. That means that patients may face large medical bills without the wherewithal to pay them. Or they may forgo care altogether because of large out-of-pocket costs.

Basically there are two types of insurance: third-party insurance and individual self-insurance. The third-party insurers are employers, insurance companies and government. Individual insurance means that people put money aside in accounts that they own and control — to be used when medical events occur.

For the well-to-do, self-insurance is easy. If they have a doctor bill they just write a check. But for families living paycheck-to-paycheck, self-insurance is not easy. That’s why Gerry Musgrave and I over 20 years ago recommended a special account (what today we call a Health Savings Account), so that the dollars will be there when they are needed.

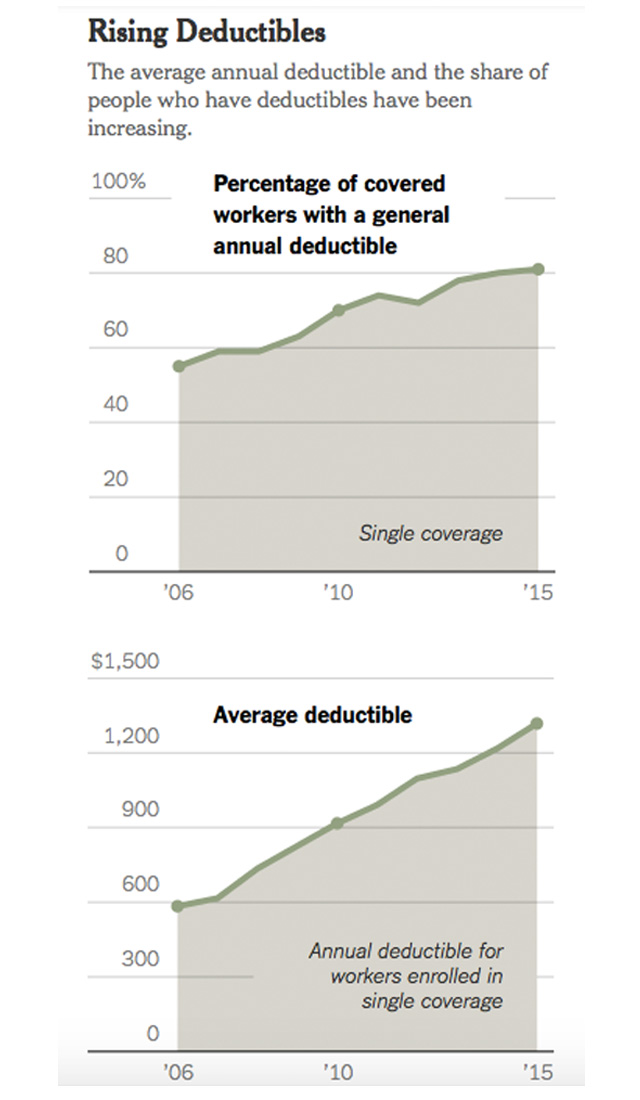

A recent Kaiser Family Foundation study identified the trend among employers. As summarized by Reed Abelson in The New York Times:

[W]orkers’ deductibles have climbed from a yearly average of $900 in 2010 for an individual plan to above $1,300 this year, while employees working for small businesses have an even higher average of $1,800 a year. One in five workers has a deductible of $2,000 or more. [See the graphs below.]

Employers in many cases are depositing funds into employee HSA accounts. But not in every case. As previously reported, the deductibles in the (ObamaCare) health insurance exchanges are about twice as high as they are in the employer plans. And although most plans sold in the exchanges are HSA compatible, I don’t know of a single case where the plan comes with an HSA deposit.

As a result, some people – both in the exchanges and at work – are facing out-of-pocket exposure of $6,600 for an individual and $13,200 for a family. For a young, healthy, low-income family, this must seem little better than being uninsured.

A Commonwealth Fund survey last year found that 40 percent of people with private health insurance whose deductible equaled 5 percent or more of their income said they avoided a doctor or a test when they were sick. This is not necessarily bad. Roughly one-third of doctor visits are probably unnecessary. And loads of tests could easily be done without.

The original RAND corporation study on the question found that when faced with high deductibles, people cut back on “necessary” and “unnecessary” care in roughly equal amounts. But these decisions had virtually no impact on health care.

Often, no one is in a better position to make the decision on whether to seek care than the patient herself. With a reasonably funded Health Savings Account, the patient will forgo care only if the expected benefits are less than the expected costs. She will not forgo care for lack of money.

How is ObamaCare affecting all of this? As I wrote previously, the Affordable Care Act is forcing millions of people to have the wrong kind of insurance. They are being required to enroll in plans that pay 100 percent of the cost for too many minor procedures of questionable value – while leaving the patient to pay out-of-pocket the full cost of items that are necessary and valuable.

To pick one example, healthy women are now entitled to free mammograms – a procedure steeped in controversy. But a woman with symptoms, who really needs a mammogram, may be forced to pay the full cost out of pocket.

ObamaCare does other things that undermine the value of HSAs and make them less useful than they could be.

I will write about that in a future column.

This article was originally posted at Forbes on October 7, 2015.

0 Comments