")

By Dr. John C. Goodman

Originally posted at Forbes, January 2017.

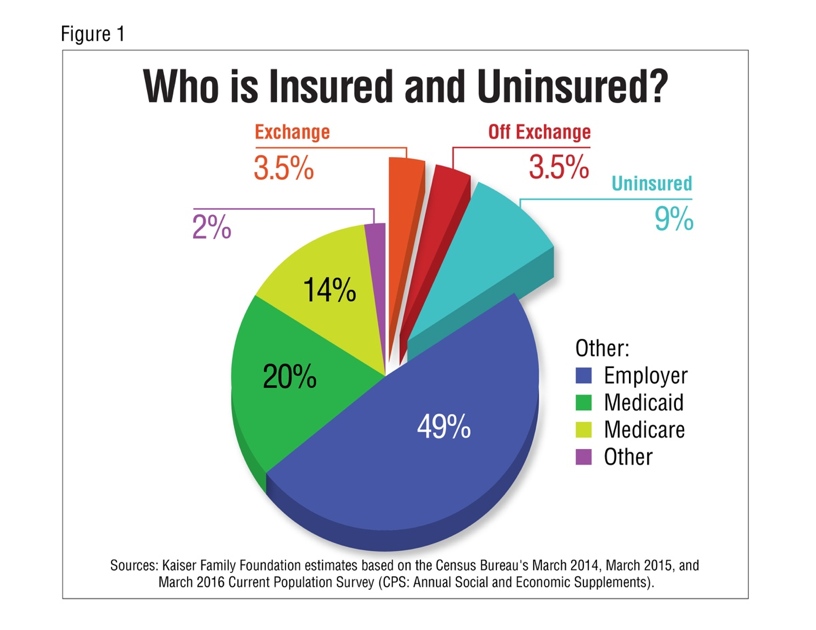

During the election campaign, Donald Trump promised to abolish Obamacare and replace it with better health reform that would not leave anyone behind. In order to understand what is implied by that promise, consider Figure I, which highlights three groups of people:

- About 11 million people are getting insurance in the exchanges and many of them are unhappy. In the words of former president Bill Clinton, many are “paying twice as much for half the coverage” they were previously enjoying.

- Another 11 million or so people are getting individual insurance outside the exchanges. These people have all the same problems as people in the exchanges. But, they receive no federal tax break for the purchase of insurance, even though a federal mandate requires them to buy it.

- In addition, about 29 million people are uninsured and that number is unlikely to change very much going forward. Polls show that the most important reason why so many people are uninsured is cost.

One way to think about Donald Trump’s campaign promise is to see that he wants to make health insurance less expensive and better for the first two groups without leaving the third group permanently uninsured. And he wants to do it with money that is already in the system. In other words, without raising taxes.

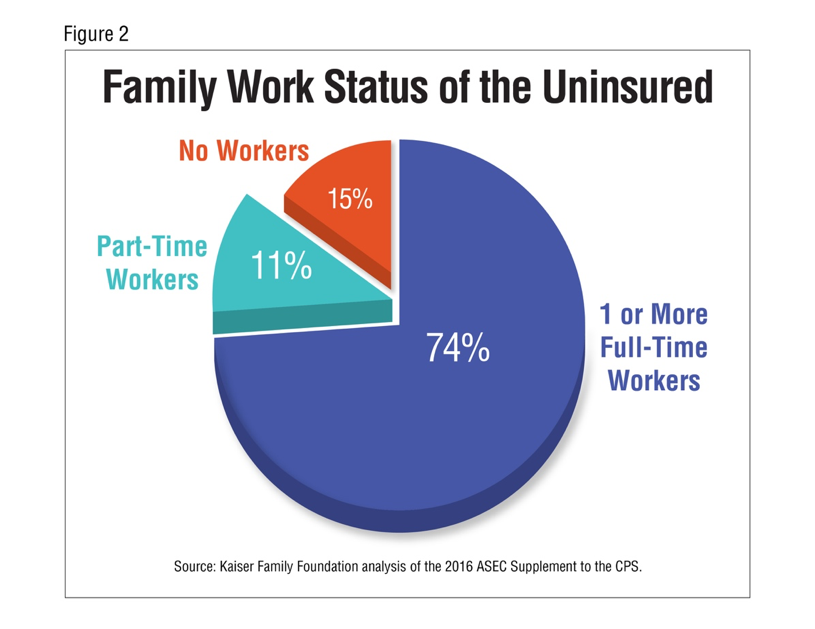

Can that be done? I believe it can. In order to see how, consider Figure II which illustrates a remarkable fact about the uninsured: 85 percent have a connection to the work place. Specifically, three fourths of the uninsured live in a household where at least one person has a full-time job and another 10 percent live in a household with a part-time worker.

That’s important to know for three reasons.

First, virtually all new government spending for private health insurance under Obamacare is going to the most dysfunctional part of the health care system – the individual market. This is where premiums are spiraling up and there is a race to the bottom on quality and access to care. Except for a very modest, very complicated and rarely used small business subsidy, Obamacare is doing nothing to encourage employers to insure more of their employees.

Second, Obamacare’s employer mandate, which tries to force employers to buy expensive insurance for their employees by threatening them with fines, is actually making things worse. Many employers are responding by offering low wage workers health plans that are unattractive and unaffordable — $6,000 deductibles and premiums that are 10% of take home pay, not including dependent coverage. As Andrew Puzder, Donald Trump’s choice for Secretary of labor has pointed out, 92% of all low-wage employees turn down these offers. This is one reason why there has been no overall change in the percent of workers getting insurance from employers. Further, when employees turn down these offers, neither they nor their dependents can get subsidized insurance in the exchanges.

Third, virtually every Republican plan to replace Obamacare, makes the same mistake Obamacare makes: they spend all of their subsidy dollars in the individual market, while making it as hard as possible for anyone with a job to actually qualify.

The exception on the Republican side is a bill introduced by Sen. Bill Cassidy (with 12 Senate co-sponsors) and bicameral legislation introduced by Rep. Pete Sessions and Sen. Cassidy. The Sessions/Cassidy proposal in particular is designed to encourage employers to help their employees get health insurance with these features:

A refundable tax credit. It is generous enough to allow access to Medicaid-like coverage at a minimum. The credit is refundable, advanceable and transferable – so it is easy for employers to do the paperwork.

Access to group insurance. If employers are willing, they can process the credit and give their employees access to the group market – especially important in states where the individual market is in a death spiral.

Access to limited benefit insurance. A partial credit is available for insurance that is especially tailored to the needs of young, healthy families with limited means (e.g., employees of the fast food industry). These families get complete financial protection, regardless of the size of their medical bills.

A reliable safety net. Unclaimed credits are made available to local safety net institutions in case any remaining uninsured cannot pay their medical bills.

Reform of the individual market. Although this may take several years, states have enormous flexibility to reform their individual markets. They can establish risk pools, reinsurance, health status risk adjustment, penalties for individuals who try to game the system, etc. They can keep the Obamacare mandates, repeal them or modify them.

Interestingly, a model for reform is the small business section of the CURES Act, which passed with huge bipartisan majorities in both houses of Congress. This legislation was mainly focused on giving patients access to life saving drugs and medical devices in the future. But it will have an immediate impact on small business (fewer than 50 employees).

- Small business can now obtain portable insurance for their employees without huge fines.

- They can choose between the individual and the group insurance markets.

- They can choose the tax regime for their employees (tax credits or the exclusion).

- They have access to a completely flexible savings account – not available to anyone else in the individual market.

- Even before the act, there was no employer mandate for these firms and if they self-insure they can have limited benefit insurance for their employees with no April 15th penalty for being uninsured.

One way to think about the Sessions/Cassidy legislation is to see that it will extend these same features to the rest of the health care system.

This article was originally published at Forbes on January 25, 2017. http://bit.ly/2ksZ5Xn

0 Comments