- John Goodman

- Larry Kotlikoff

- Jane Shaw Stroup

- Thomas Saving

- Devon Herrick

- Linda Gorman

- Pete Du Pont

- All Posts

Is There a Trump Health Care Plan?

Although he rarely talks about it, the most significant gift Donald Trump bequeathed to economic prosperity was deregulation. And the one sector that was deregulated more than any other was health care. Since Joe Biden has been re-regulating the economy, it’s hard to think of a starker contrast between the two leading presidential candidates this year – and it affects all aspects of health care. More

Liberalism Explained

In the early 20th century, they called themselves “progressives.” Then, they were “liberals.” Now they are “progressives” again. Early on, they embraced racism and endorsed eugenics. Then they became advocates for civil rights. Now they endorse racism of a different sort – wokeness. If you had to the describe the distinguishing characteristic of modern liberalism, what would your answer be? John Goodman gives a novel answer. More

Social Security Reform, Part II

To get seniors to support Social Security reform, there are additional abuses that need correcting. These include: stopping the double taxation of senior income through the Social Security benefits tax, no longer forcing seniors to dissave, abolishing the Social Security earnings penalty, and ending taxation by inflation. More

Obamacare Exchanges at Age Ten

March 23rd will mark the 14th anniversary of the Affordable Care Act, and it is now ten years since the creation of the Obamacare exchanges. There are three ways to look at Obamacare today: in terms of (1) what the Obama administration said it was about, (2) what policy wonks thought it was about, and (3) how it really works. More at my post at Forbes.

How to Reform Social Security

The key to reform is to make today’s retirees positive beneficiaries of reform.

A golden opportunity to do so exists for two reasons: (1) the current system is abusing senior retirees in myriad ways, and (2) many of these abuses can be eliminated without any cost to the Treasury. In other words, some aspects of responsible reform are a free lunch.

California Dreaming

California legislators want the state to provide free health care to every resident, including undocumented immigrants. Under the act, it would be illegal for any resident to pay a doctor privately for any medical treatment covered by CalCare. John Goodman and Linda Gorman predict higher taxes, less choice, an exodus of doctors and nurses out of the state, rationing by waiting, and something actually worse than Medicaid for all. See our editorial in the Orange County Register.

What’s Wrong with the US Welfare State?

The bottom fifth of households in 2017 had an average (after tax and after entitlement spending) income of $33,653 per person. Almost all of this “income” is in the form of noncash welfare benefits. If all those benefits were converted into cash, a family of four in the bottom fifth of the (earned) income distribution would have $134,652 a year to spend, after taxes! The bottom fifth also had more per capita “income” than the next fifth and the middle fifth. To answer the question, “What’s Wrong?” I really shouldn’t have to say anything more. But, I did find a few more things to say in my most recent post at Forbes.

What To Do About Our Biggest Health Care Problems

Short-term health insurance and indemnity insurance are meeting needs not met by Obamacare. You would appreciate why that is a good thing if you understand:

Goodman’s Rule for Rational Public Policy: Let the markets handle all the problems markets can solve; and turn to government only to meet needs that competitive markets cannot or do not meet.

Is There a Trump Health Care Plan?

Although he rarely talks about it, the most significant gift Donald Trump bequeathed to economic prosperity was deregulation. And the one sector that was deregulated more than any other was health care. Since Joe Biden has been re-regulating the economy, it’s hard to think of a starker contrast between the two leading presidential candidates this year – and it affects all aspects of health care. More

Liberalism Explained

In the early 20th century, they called themselves “progressives.” Then, they were “liberals.” Now they are “progressives” again. Early on, they embraced racism and endorsed eugenics. Then they became advocates for civil rights. Now they endorse racism of a different sort – wokeness. If you had to the describe the distinguishing characteristic of modern liberalism, what would your answer be? John Goodman gives a novel answer. More

Is There a Trump Health Care Plan?

Although he rarely talks about it, the most significant gift Donald Trump bequeathed to economic prosperity was deregulation. And the one sector that was deregulated more than any other was health care. Since Joe Biden has been re-regulating the economy, it’s hard to think of a starker contrast between the two leading presidential candidates this year – and it affects all aspects of health care. More

ObamaCare still desperately needs fixing

The American Rescue Plan injects new life into ObamaCare with more generous subsidies, expanded eligibility and premium limits that make insurance more affordable. Unfortunately, the stimulus proposal just passed by Congress does nothing to correct the most serious...

The Government’s New Tax Break for Retirees is Less Than Meets the Eye

QLACs — Qualified Longevity Annuity Contracts promise to be “A Retirement Tax Break That Ends the Fear of Outliving Your 401(k).” But while buying a QLAC lowers the person’s exposure to one major risk (living too long), it raises exposure to another risk: inflation. More

What the Debt Deal Ignored

A month ago, Social Security’s Trustees published their annual report. Table VIF1, buried deep in the Appendix, where no one looks, is the statement that Social Security’s unfunded liability is $66 trillion. This measure of Social Security’s red ink is not just gargantuan on its own. It’s $13 trillion larger than it was just three years ago. More

Social Security Sues invalid for Money He Received 21 Years Ago, At Age 11

Roy Farmer of Grand Rapids Michigan has Cerebral Palsy. He’s 32. In 2019, out of the blue, he received a claw back letter from Social Security demanding he repay $4,902 that his (now deceased) mother received back when he was 11. Roy has spent over three years appealing this judgement. He’s been denied twice. More from Kotlikoff Forbes editorial.

Our Fiscal System Needs Reform

Over half of working-age Americans face lifetime marginal tax rates (including direct taxes and loss of entitlement benefits) above 43 percent. One in ten in the bottom fifth face tax rates above 70 percent, effectively locking them into poverty. For some would-be-workers, the tax rates exceed 100 percent.

Extremely high LMTRs reflect the complete loss of family benefits, in the current and future years, from programs such as Medicaid – which ends benefits abruptly if one’s income or assets exceed specific thresholds by even one dollar. More.

Social Security’s Massive Malfeasance

Social Security has committed and continues to commit huge fraud against 13,000 plus widow(er)s who collectively have been swindled out of $130 million. Those are the figures of Social Security’s own Inspector General. More

America’s Fiscal Gap

That’s the difference between the federal government’s spending commitments and its income – looking indefinitely into the future. Closing the gap through time requires an immediate and permanent 41.3 percent increase in all federal taxes or an immediate and permanent 35.3 percent cut in all non interest federal spending. More

Social Security Benefits: Heads They Win, Tails You Lose

One disabled lady was clawed back for over $300,000 for a mistake that Social Security admitted in writing was theirs! If she doesn’t repay, Social Security will almost always stop sending people like her a single penny until they pay “what they owe.” This can take years or decades. More

ObamaCare still desperately needs fixing

The American Rescue Plan injects new life into ObamaCare with more generous subsidies, expanded eligibility and premium limits that make insurance more affordable. Unfortunately, the stimulus proposal just passed by Congress does nothing to correct the most serious...

The Government’s New Tax Break for Retirees is Less Than Meets the Eye

QLACs — Qualified Longevity Annuity Contracts promise to be “A Retirement Tax Break That Ends the Fear of Outliving Your 401(k).” But while buying a QLAC lowers the person’s exposure to one major risk (living too long), it raises exposure to another risk: inflation. More

ObamaCare still desperately needs fixing

The American Rescue Plan injects new life into ObamaCare with more generous subsidies, expanded eligibility and premium limits that make insurance more affordable. Unfortunately, the stimulus proposal just passed by Congress does nothing to correct the most serious...

More Important Than the Industrial Revolution

It’s called the Transportation-Communication Revolution. In recent times, shipping costs have fallen by 50 percent and air cargo costs have fallen by almost 100 percent. As a result, the per capita GDP of developing countries (outside of sub-Saharan Africa) between 1960 and 2015 rose a whopping 549 percent.

Julian Simon, Vindicated Again

Each year, the Competitive Enterprise Institute (CEI) has a dinner in Washington, D.C., honoring the economist Julian Simon, who died in 1998. Simon was a rare optimist in the fields of population and natural resources. He disagreed with most environmentalists of his day (especially in the 1980s through 1990s). They feared passionately that growing population would overwhelm agriculture and industry and that the world would run out of natural resources such as oil and minerals.

The “Madness of Crowds”?

Can history help us understand today’s panic over global warming? While the Earth is warming and human activity is probably contributing to it, the overheated efforts to make people fear the long-term future suggest that this is more of a crusade than a rationally considered enterprise. Extreme fear of global warming is negatively affecting politics, the economy, the media, international relations, and education.

Economic Growth Theories Fall into the Dustbin of History (And That’s Okay)

Economists like Samuelson failed to understand economic growth in developing countries. Unbeknownst to them, cost-reducing innovations in transportation and communication led to increased trade and lifted people out of poverty. The Industrial Revolution benefited only a small portion of the world. Trade spurred prosperity and development on its own.

Conservation Leases?

This guest post by Shawn Regan is a substantive analysis of the recent proposal by the Interior Department's Bureau of Land Management to allow leasing of public land for conservation purposes. Regan is vice president of research at the Property and Environment...

Can There Be Too Many Trees?

Drought-resistant trees are replacing grasslands around the world, and, specifically in the western United States. This is a problem? More.

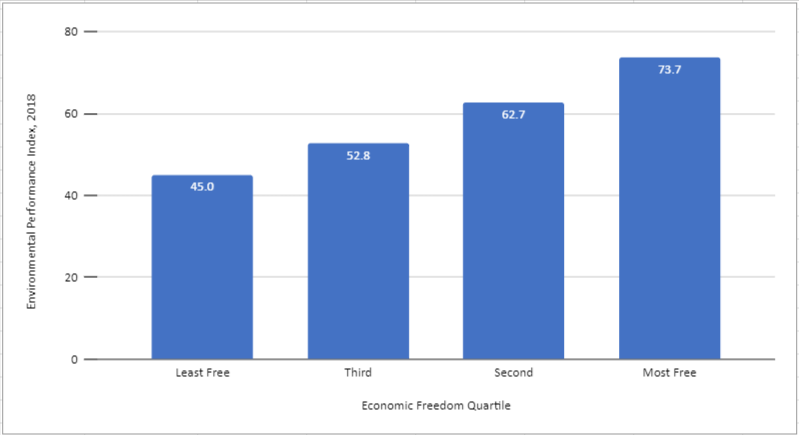

Economic Freedom IS good for the environment

Yes, data from the Yale Center for Environmental Law & Policy and the Fraser Institute’s Economic Freedom of the World Index send a resounding message: Economic freedom brings about environmental protection. Why? Because economic freedom leads to prosperity and only prosperous countries can truly protect their environment. Are you skeptical? More.

Why California Needs Higher Prices for Water

California’s extreme drought will force rationing of water or higher prices, say John McKenzie and Richard McKenzie. Raising water prices has a great advantage: “Higher water prices can increase the state’s available water supply—without additional rainfall or...

More Important Than the Industrial Revolution

It’s called the Transportation-Communication Revolution. In recent times, shipping costs have fallen by 50 percent and air cargo costs have fallen by almost 100 percent. As a result, the per capita GDP of developing countries (outside of sub-Saharan Africa) between 1960 and 2015 rose a whopping 549 percent.

Julian Simon, Vindicated Again

Each year, the Competitive Enterprise Institute (CEI) has a dinner in Washington, D.C., honoring the economist Julian Simon, who died in 1998. Simon was a rare optimist in the fields of population and natural resources. He disagreed with most environmentalists of his day (especially in the 1980s through 1990s). They feared passionately that growing population would overwhelm agriculture and industry and that the world would run out of natural resources such as oil and minerals.

More Important Than the Industrial Revolution

It’s called the Transportation-Communication Revolution. In recent times, shipping costs have fallen by 50 percent and air cargo costs have fallen by almost 100 percent. As a result, the per capita GDP of developing countries (outside of sub-Saharan Africa) between 1960 and 2015 rose a whopping 549 percent.

Savings and Gramm: How the Fed is Slowing Monetary Growth

The Federal Reserve is buying Treasury bills and mortgage-backed securities at a rate of $120 billion a month. This is apparently being done to support large borrowing by the federal government. At the same time, the Fed has pulled almost a trillion dollars of liquidity out of the financial system by “reverse-repo borrowing.” This has reduced bank reserves and private sector lending. Not surprisingly, the growth of the M2 money stock fell from around 25% in 2020 to around 10% on an annualized basis in the first six months of 2021.

Gramm and Saving in the WSJ: The Fed has lost its ability to control interest rates

Writing in the Wall Street Journal, former Sen. Phil Gramm and Goodman institute Senior Fellow Thomas Saving write “Never in the Fed’s 105-year history has it had less control over market interest rates than it has today…. To expect the Fed to hold interest rates above or below the market rate under these circumstances is not only naive but dangerous.”

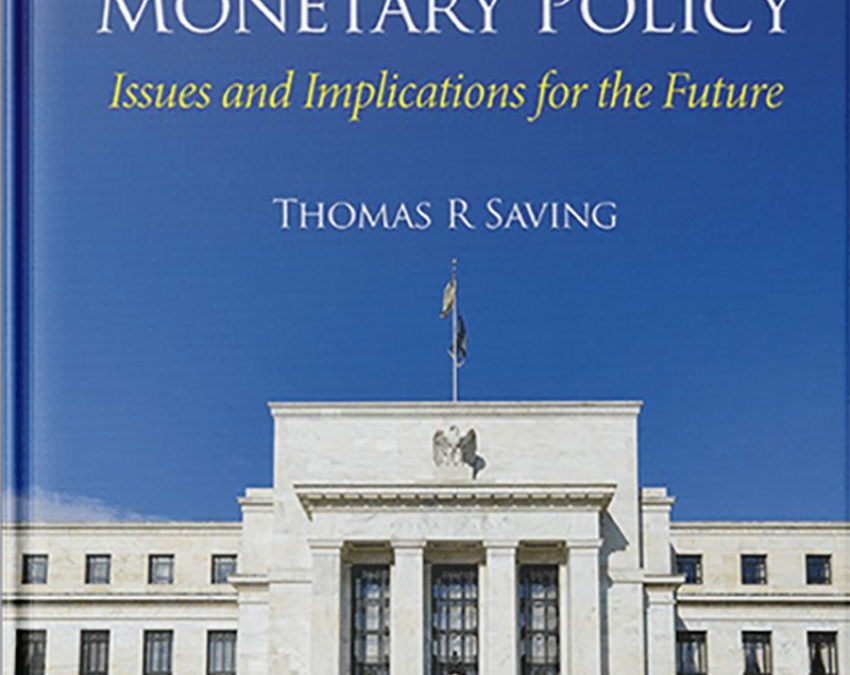

Tom Saving has a new book

Tom Saving has a new book called A Century of Federal Reserve Monetary Policy: Issues and Implications for the Future.

Saving and Gramm in the Wall Street Journal: The Fed’s Obama-Era Hangover

The Federal Reserve System is paying banks not to lend money under an Obama era policy.

Goodman and Saving: Budget Deal’s Trillion Dollar Surprise

The most significant federal entitlement reform in our lifetime was a little noticed provision that Democrats included in the Affordable Care Act. The provision was a cap on Medicare spending, similar to the cap Republicans proposed for Medicaid last summer.

Saving on CNBC: FED is holding 20% of federal debt

The Federal Reserve System is holding 20% of the federal government’s publicly held debt. It also is holding a lot of bank reserves. For every dollar of required reserves, banks have deposited $12 at the FED.

Gramm and Saving in the Wall Street Journal: Fed Task is Precarious

The Fed balance sheet contains 20% of all publicly held federal debt and 34% of the value of all outstanding government-guaranteed mortgage-backed securities. As the economy returns to normal growth, getting rid of those assets risks runaway inflation or a crippled recovery or both.

Saving: Are Republicans Too Stingy with Medicaid?

Before the Senate voted on a “skinny” alternative to Obamacare, it was considering the House version of repeal and replace – called the Better Care Reconciliation Act (BCRA).

Savings and Gramm: How the Fed is Slowing Monetary Growth

The Federal Reserve is buying Treasury bills and mortgage-backed securities at a rate of $120 billion a month. This is apparently being done to support large borrowing by the federal government. At the same time, the Fed has pulled almost a trillion dollars of liquidity out of the financial system by “reverse-repo borrowing.” This has reduced bank reserves and private sector lending. Not surprisingly, the growth of the M2 money stock fell from around 25% in 2020 to around 10% on an annualized basis in the first six months of 2021.

Gramm and Saving in the WSJ: The Fed has lost its ability to control interest rates

Writing in the Wall Street Journal, former Sen. Phil Gramm and Goodman institute Senior Fellow Thomas Saving write “Never in the Fed’s 105-year history has it had less control over market interest rates than it has today…. To expect the Fed to hold interest rates above or below the market rate under these circumstances is not only naive but dangerous.”

Savings and Gramm: How the Fed is Slowing Monetary Growth

The Federal Reserve is buying Treasury bills and mortgage-backed securities at a rate of $120 billion a month. This is apparently being done to support large borrowing by the federal government. At the same time, the Fed has pulled almost a trillion dollars of liquidity out of the financial system by “reverse-repo borrowing.” This has reduced bank reserves and private sector lending. Not surprisingly, the growth of the M2 money stock fell from around 25% in 2020 to around 10% on an annualized basis in the first six months of 2021.

The Perils of Trying to Become a Doctor

This week the National Resident Matching Program (Match) will inform between 45,000 to 50,000 medical graduates whether they have a career in medicine or should try for Plan B. Some of those who failed to match (about 20 percent) will spend the rest of their lives trying to pay down $300,000 in medical school debt without an income capable of servicing that debt.

How a Questionable Drug Turned into a Goldmine at Taxpayers’ Expense

On June 7th the U.S. Food and Drug Administration approved a new drug to treat early-stage Alzheimer’s disease. Is this good news for patients suffering with Alzheimer’s disease? Probably not and certainly not for taxpayers. The clinical trial data found little evidence the drug works. One Phase 3 clinical trial showed a slight slowing in cognitive decline, while the second clinical trial failed to show any improvement.

What’s Behind the Vaccine Slowdown?

What’s behind the slowdown in vaccinations? The consensus among experts is those not yet vaccinated either 1) don’t want the vaccine 2) harbor some doubts about vaccine safety or efficacy, or 3) simply lack the motivation to find vaccine providers and make an appointment. Vaccine hesitancy accounts for about one-third of adults. For example, the Kaiser Family Foundation ran a survey in April that found 15 percent of respondents who had not received the vaccine plan to “wait and see.” Another 6 percent will get vaccinated “only if required,” and 13 percent refuse to get the vaccine.

Correcting Misconceptions of Health Care Reform

One reader posed the question, how does the tax break for employee health insurance harm our health care system? Short answer: over time the practice reduced competition, which weakened cost-control and resulted in health care inflation three times that of consumer inflation. Consider this: once covered by generous health plans, workers cared less about what medical care cost because their health plans paid most of the tab. Employers didn’t care what things cost because they were passing on the costs to workers (indirectly) in lieu of higher cash wages. Third party administrators (TPAs), who manage the benefits for employers, didn’t much care what things cost because they were passing on the costs to employers with a mark-up. The more money spent, the more TPAs earn.

Health Reform: There Is Something for Everyone to Love… and Hate

Why is it controversial to expand the physician supply, creating more competition? Doctors oppose it, just like they oppose expanding the scope of practice for nurse practitioners. Doctors don’t want me to be able to see a nurse practitioner or physician assistant for a wart on my toe unless that NP/PA works for them.

How did doctors get so powerful? In the first half of the 20th Century, the American Medical Association (AMA) waged a largely successful battle to close medical schools that trained competing physicians. …. More than half of American and Canadian medical schools were closed…. Thus, the job of a physician was yanked out of reach of all but the smartest, most disciplined, wealthy elites.

The 60 Percent Solution to Reforming Healthcare

Can we transform the entire health care system by empowering the roughly 60 percent of patients who are in private health plans? That’s the premise of a new book I just read by Todd Furniss (@TFurniss on Twitter). The author ofThe 60% Solution: Rethinking Healthcare, believes there are five major reforms necessary to empower patients and help them get better care at better prices. These include: (1) change governance, (2) modify health savings accounts (HSAs), (3) clear prices, (4) standardize accounting and information technology in the medical industry and (5) emphasize primary care.

Herrick: OBAMACARE RATIONS CARE FOR THE SICK AND OVERCHARGES THE HEALTHY

The health care reform debate that lead to Obamacare was initially about covering the uninsured, but in order to gain the support of ordinary people who already had coverage, proponents had to figure out a way to sway public opinion.

Herrick: States Should Ban These Lab Scams

There is a new health care scam spreading across rural America that could cost you plenty. Large commercial labs like Quest Diagnostics and LabCorp do not have locations in every small town. As a result, many rural hospitals perform lab work for both their inpatients and outpatients in the local community.

The Perils of Trying to Become a Doctor

This week the National Resident Matching Program (Match) will inform between 45,000 to 50,000 medical graduates whether they have a career in medicine or should try for Plan B. Some of those who failed to match (about 20 percent) will spend the rest of their lives trying to pay down $300,000 in medical school debt without an income capable of servicing that debt.

How a Questionable Drug Turned into a Goldmine at Taxpayers’ Expense

On June 7th the U.S. Food and Drug Administration approved a new drug to treat early-stage Alzheimer’s disease. Is this good news for patients suffering with Alzheimer’s disease? Probably not and certainly not for taxpayers. The clinical trial data found little evidence the drug works. One Phase 3 clinical trial showed a slight slowing in cognitive decline, while the second clinical trial failed to show any improvement.

The Perils of Trying to Become a Doctor

This week the National Resident Matching Program (Match) will inform between 45,000 to 50,000 medical graduates whether they have a career in medicine or should try for Plan B. Some of those who failed to match (about 20 percent) will spend the rest of their lives trying to pay down $300,000 in medical school debt without an income capable of servicing that debt.

California Dreaming

California legislators want the state to provide free health care to every resident, including undocumented immigrants. Under the act, it would be illegal for any resident to pay a doctor privately for any medical treatment covered by CalCare. John Goodman and Linda Gorman predict higher taxes, less choice, an exodus of doctors and nurses out of the state, rationing by waiting, and something actually worse than Medicaid for all. See our editorial in the Orange County Register.

Leftists in Colorado Seem Poised to Try Again for Single Payer Health Insurance

Last time around, the idea was rejected by almost 79% of the voters. And for good reasons. British Columbia’s single payer system is so mismanaged it pays for cancer patient radiation treatments in Bellingham, Washington. Its hip replacement wait can be almost a year… Because Canadian patients wait twice as long as recommended for MRI scans, those who can afford it pay cash for quick service at US imaging centers in border cities like Buffalo, NY and Bellevue, WA. More.

Against Medicaid Expansion

Expanding Medicaid to the relatively healthy might make sense if it improved general health. But there is little evidence it does. In Oregon, for example, a first-of-its-kind controlled trial tracked individuals who applied for Medicaid through a lottery. After two years, there was no discernible difference in the physical health of the winners and losers. More

Hidden Traps in the IRA Bill’s Drug Provisions

In the near future, the elderly and the disabled will face a double whammy: higher premiums for Part D drug insurance and higher prices at the pharmacy. This is on top of negotiated prices (and the consequent drop in new drug production) which will kick in later in the decade.

John Goodman and Linda Gorman explain why this will happen in The Hill.

The $3.5T Spending Mistake

Congressional Democrats are proposing to spend an enormous amount of taxpayer dollars on what the New York Times calls a “cradle to the grave” addition to U.S. social welfare. When budgeting shenanigans are ignored, the Committee for a Responsible Federal Budget estimates that the full cost is not the $3.5 trillion that has been widely advertised, but at least $5.0 trillion and possibly as much as $5.5 trillion.

Gorman: US Hospitals are Safer

A frequent criticism of US hospitals is the charge of excessive adverse medical events, sometimes leading to avoidable deaths. How do our hospitals compare to hospitals in national health care systems? Quite well. The percent of patients who experience an adverse event is twice as high in Canada, three times as high in Britain and four times as high in New Zealand.

If The Court Strikes Down Obamacare, How Bad Would That Be?

This article was coauthored by Linda Gorman, director of health care at the Independence Institute in Denver, Colorado.

Gorman in The Hill: Trump’s Drug Plan Wrong Rx

The Trump administration wants to use an average of the drug prices paid by other countries to limit what Medicare Part B pays for some drugs. This is a bad idea.

California Dreaming

California legislators want the state to provide free health care to every resident, including undocumented immigrants. Under the act, it would be illegal for any resident to pay a doctor privately for any medical treatment covered by CalCare. John Goodman and Linda Gorman predict higher taxes, less choice, an exodus of doctors and nurses out of the state, rationing by waiting, and something actually worse than Medicaid for all. See our editorial in the Orange County Register.

Leftists in Colorado Seem Poised to Try Again for Single Payer Health Insurance

Last time around, the idea was rejected by almost 79% of the voters. And for good reasons. British Columbia’s single payer system is so mismanaged it pays for cancer patient radiation treatments in Bellingham, Washington. Its hip replacement wait can be almost a year… Because Canadian patients wait twice as long as recommended for MRI scans, those who can afford it pay cash for quick service at US imaging centers in border cities like Buffalo, NY and Bellevue, WA. More.

California Dreaming

California legislators want the state to provide free health care to every resident, including undocumented immigrants. Under the act, it would be illegal for any resident to pay a doctor privately for any medical treatment covered by CalCare. John Goodman and Linda Gorman predict higher taxes, less choice, an exodus of doctors and nurses out of the state, rationing by waiting, and something actually worse than Medicaid for all. See our editorial in the Orange County Register.

Farewell

Some thoughts on the views that have animated this column. By Pete du Pont May 27, 2014 Source: The Wall Street Journal This will be the last of my columns for this publication, so I thought it fitting to note the views that have most influenced these writings....

The Real Inequality Problem

It isn’t that some people are wealthy but that others are struggling. Commentary by Pete du Pont April 28, 2014 Source: The Wall Street Journal Among the too numerous frustrations of the political process is that a lot of smart and talented people spend their time and...

The Left’s “Wars”

The Left’s “Wars” Commentary by Pete du Pont March 28, 2014 Source: The Wall Street Journal The midterm elections are just over seven months away and the left has unleashed its usual rhetoric about the Republican "war on women." It's baseless political pandering of...

Global Warming Heats Up

The public could use an honest debate. Commentary by Pete du Pont February 27, 2014 Source: The Wall Street Journal Global warming is back. Not actual global warming, as the decadelong trend of little to no increase in temperatures continues. But the topic of global...

Our Gravest Peril

ObamaCare? Stagnant economy? Crushing debt? Foreign policy fecklessness may trump them all. Commentary by Pete du Pont January 21, 2014 Source: Wall Street Journal America's most worrisome problem may not be the failed takeover of our healthcare system. It may not be...

The Great Destroyer

ObamaCare wreaks havoc on health care, the economy, American freedom and Obama's presidency. Commentary by Pete du Pont November 25, 2013 Source:The Wall Street Journal Polls show an increasing majority of Americans dislike President Obama's healthcare law and...

Hillary Will Run

How could she not? Commentary by Pete du Pont October 29, 2013 Source: Wall Street Journal Hillary Clinton is going to run for president in 2016. Granted, she is exhibiting even more coyness than most presidential prospects, and yes, the media are filled with those...

The Beltway Stalemate

Democrats and Republicans have never had such a conflict of visions. Commentary by Pete du Pont September 26, 2013 Source: The Wall Street Journal The debate about military action in Syria seems over for now, and Washington is back in campaign mode. We have a...

Farewell

Some thoughts on the views that have animated this column. By Pete du Pont May 27, 2014 Source: The Wall Street Journal This will be the last of my columns for this publication, so I thought it fitting to note the views that have most influenced these writings....

The Real Inequality Problem

It isn’t that some people are wealthy but that others are struggling. Commentary by Pete du Pont April 28, 2014 Source: The Wall Street Journal Among the too numerous frustrations of the political process is that a lot of smart and talented people spend their time and...

Farewell

Some thoughts on the views that have animated this column. By Pete du Pont May 27, 2014 Source: The Wall Street Journal This will be the last of my columns for this publication, so I thought it fitting to note the views that have most influenced these writings....

Is There a Trump Health Care Plan?

Although he rarely talks about it, the most significant gift Donald Trump bequeathed to economic prosperity was deregulation. And the one sector that was deregulated more than any other was health care. Since Joe Biden has been re-regulating the economy, it’s hard to think of a starker contrast between the two leading presidential candidates this year – and it affects all aspects of health care. More

Liberalism Explained

In the early 20th century, they called themselves “progressives.” Then, they were “liberals.” Now they are “progressives” again. Early on, they embraced racism and endorsed eugenics. Then they became advocates for civil rights. Now they endorse racism of a different sort – wokeness. If you had to the describe the distinguishing characteristic of modern liberalism, what would your answer be? John Goodman gives a novel answer. More

Social Security Reform, Part II

To get seniors to support Social Security reform, there are additional abuses that need correcting. These include: stopping the double taxation of senior income through the Social Security benefits tax, no longer forcing seniors to dissave, abolishing the Social Security earnings penalty, and ending taxation by inflation. More

Obamacare Exchanges at Age Ten

March 23rd will mark the 14th anniversary of the Affordable Care Act, and it is now ten years since the creation of the Obamacare exchanges. There are three ways to look at Obamacare today: in terms of (1) what the Obama administration said it was about, (2) what policy wonks thought it was about, and (3) how it really works. More at my post at Forbes.

How to Reform Social Security

The key to reform is to make today’s retirees positive beneficiaries of reform.

A golden opportunity to do so exists for two reasons: (1) the current system is abusing senior retirees in myriad ways, and (2) many of these abuses can be eliminated without any cost to the Treasury. In other words, some aspects of responsible reform are a free lunch.

California Dreaming

California legislators want the state to provide free health care to every resident, including undocumented immigrants. Under the act, it would be illegal for any resident to pay a doctor privately for any medical treatment covered by CalCare. John Goodman and Linda Gorman predict higher taxes, less choice, an exodus of doctors and nurses out of the state, rationing by waiting, and something actually worse than Medicaid for all. See our editorial in the Orange County Register.

More Important Than the Industrial Revolution

It’s called the Transportation-Communication Revolution. In recent times, shipping costs have fallen by 50 percent and air cargo costs have fallen by almost 100 percent. As a result, the per capita GDP of developing countries (outside of sub-Saharan Africa) between 1960 and 2015 rose a whopping 549 percent.

What’s Wrong with the US Welfare State?

The bottom fifth of households in 2017 had an average (after tax and after entitlement spending) income of $33,653 per person. Almost all of this “income” is in the form of noncash welfare benefits. If all those benefits were converted into cash, a family of four in the bottom fifth of the (earned) income distribution would have $134,652 a year to spend, after taxes! The bottom fifth also had more per capita “income” than the next fifth and the middle fifth. To answer the question, “What’s Wrong?” I really shouldn’t have to say anything more. But, I did find a few more things to say in my most recent post at Forbes.

Is There a Trump Health Care Plan?

Although he rarely talks about it, the most significant gift Donald Trump bequeathed to economic prosperity was deregulation. And the one sector that was deregulated more than any other was health care. Since Joe Biden has been re-regulating the economy, it’s hard to think of a starker contrast between the two leading presidential candidates this year – and it affects all aspects of health care. More

Liberalism Explained

In the early 20th century, they called themselves “progressives.” Then, they were “liberals.” Now they are “progressives” again. Early on, they embraced racism and endorsed eugenics. Then they became advocates for civil rights. Now they endorse racism of a different sort – wokeness. If you had to the describe the distinguishing characteristic of modern liberalism, what would your answer be? John Goodman gives a novel answer. More

Is There a Trump Health Care Plan?

Although he rarely talks about it, the most significant gift Donald Trump bequeathed to economic prosperity was deregulation. And the one sector that was deregulated more than any other was health care. Since Joe Biden has been re-regulating the economy, it’s hard to think of a starker contrast between the two leading presidential candidates this year – and it affects all aspects of health care. More